The aftermath of the recession and the reaction and relaunch measures of businesses

What emerges through the official statistics and specially-made estimates offer us a broad picture of the audiovisual sector rebound during the health crisis – a difficult picture that deserves updated and further study.

This chapter investigates the effects of the crisis on the sector, looking into the operating methods of businesses during the various phases (lockdown and resumption) and the strategies adopted to contrast and relaunch regular activities. To do so, a questionnaire was submitted to 600 companies during the first half of October, and the data were processed.

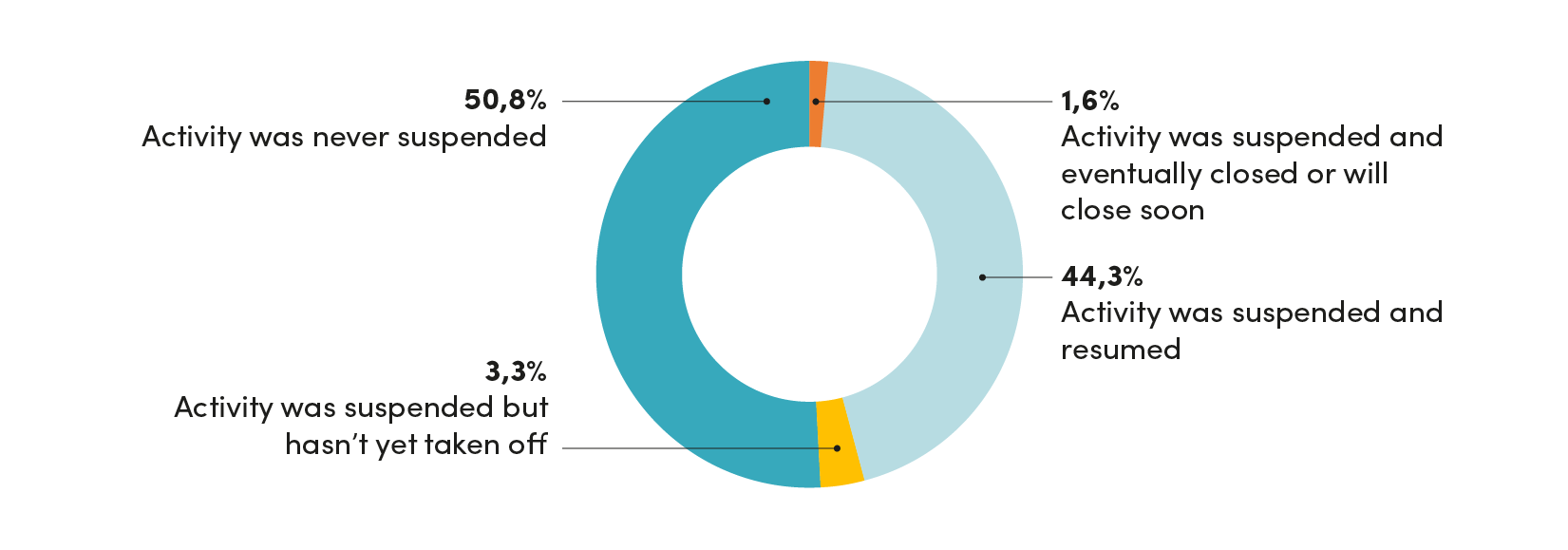

Based on the answers, half of the interviewees (50.8%) asserted they weren’t subjected to restrictions during the lockdown and did not need to close, despite the difficulties encountered.

However, 44.3% said they had been forced to close due to Covid in Phase 1; a residual 5% never opened again after the initial shutdown, either by choice (3.3%) or because their closure was already planned (1.6%).

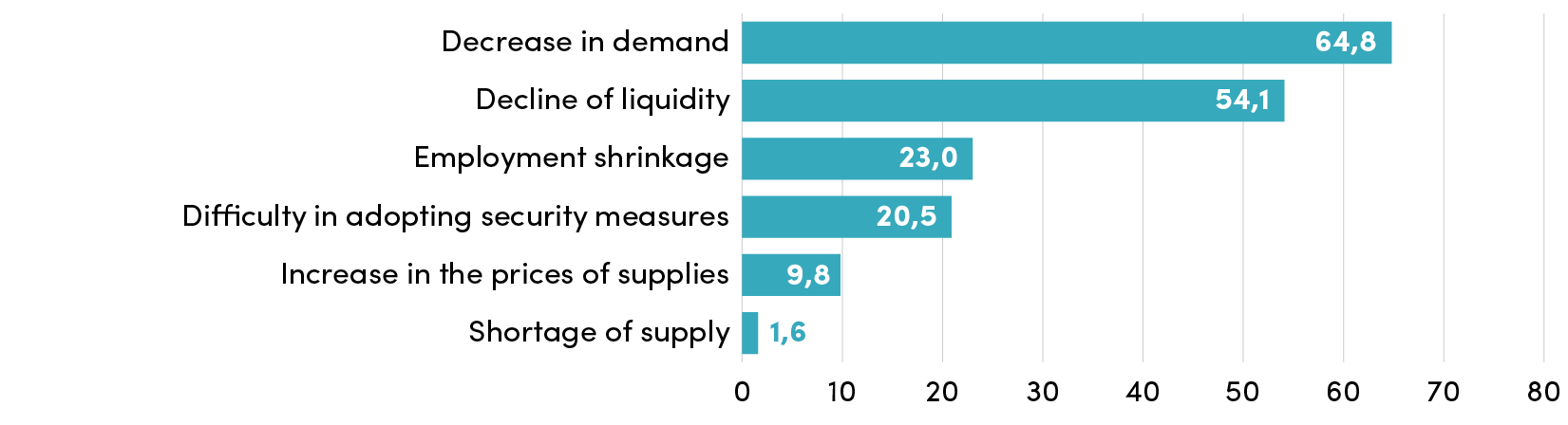

Regardless of the activity condition, over 90% of the companies interviewed asserted one or more difficulties arose from the health crisis. Two-thirds of the sector pointed to the decrease in demand as one of the main problems, and the resulting fall in liquidity (54.1%) represents an obstacle that policymakers cannot ignore. Subsequently, the inability to maintain employment levels (23.0%) and the difficulty in adopting measures to fight the spread of the disease (20.5%) were key elements to the critical condition of businesses.

Graphic 1 – Audiovisual core businesses in 2020: operating conditions

Year 2020 (in percentage)

Source: Symbola Foundation survey

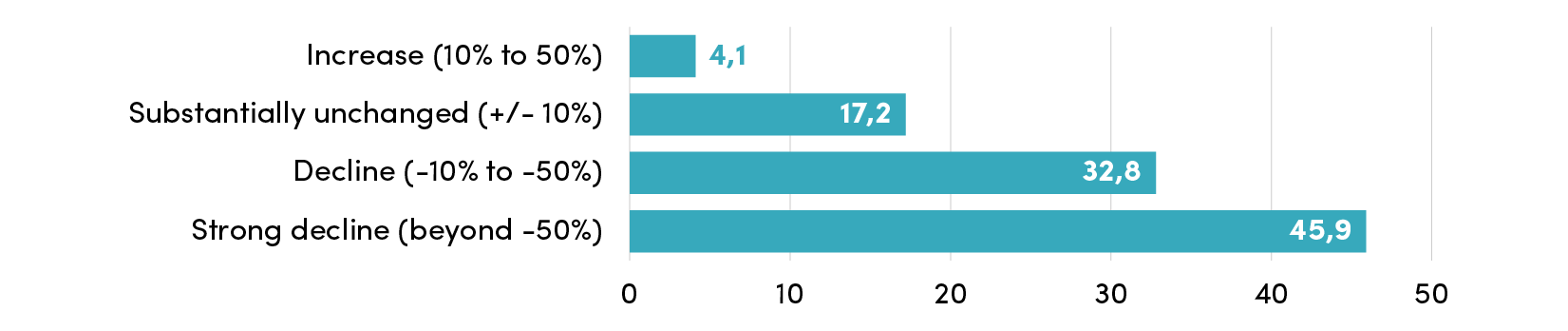

The fall of liquidity and the decrease in demand are reflected in a deadweight loss of turnover, leading to a series of indirect effects. As initially foreseen by many analysts, the loss of business volume resulting from the generalized shutdown should have produced a technical resumption capable of recovering much of the lost ground. However, this was not the case, and it can be seen both from the preliminary data on the general economy and from the specific indications of the audiovisual industry. This can be easily understood by analyzing the answers for the two investigated phases (shutdown/Phase 1 and resumption/Phase 2). In Phase 1, 45.9% declared they had more than halved their turnover compared to the same period of the previous year.

Graphic 2 – Businesses’ criticalities following the health emergency

Year 2020 (in percentage; multiple answers possible)

Source: Symbola Foundation survey

32.8% placed the turnover dynamics in a range from -10% to -50%, for a total of almost 4 out of 5 companies suffering a significant decrease in business volume. Of the audiovisual companies interviewed, only less than 20% showed signs of resilience to the health crisis, of which 4.1% even registered an increase, in contrast to the rest of the sector and the economy.

Graphic 3 – Turnover trend during Phase 1 compared to the previous year

Year 2020 (in percentage)

Source: Symbola Foundation survey

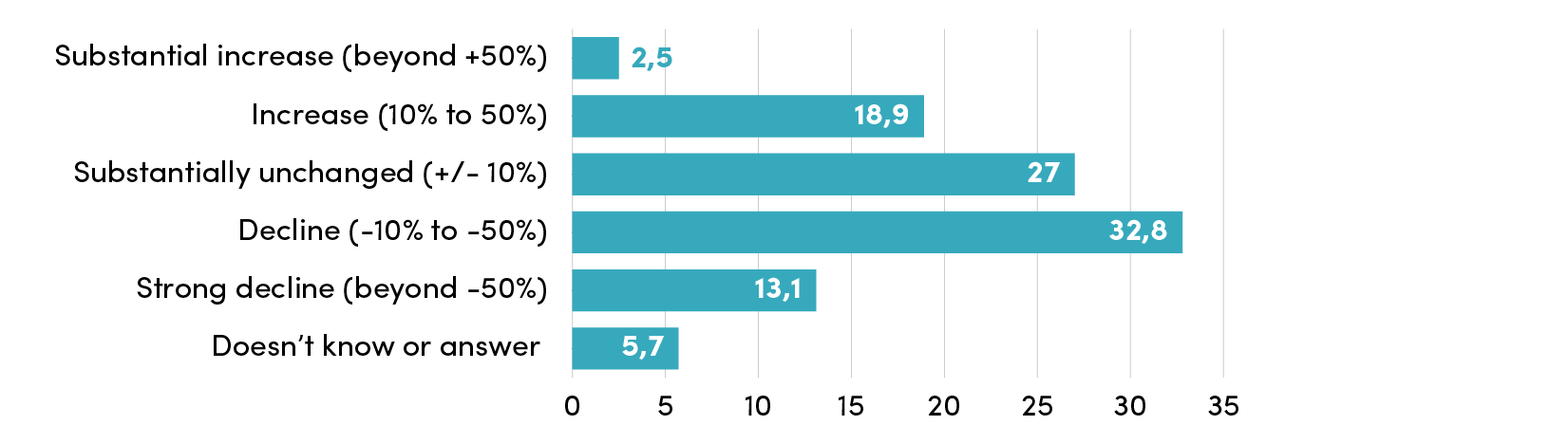

The resumption of activities (Phase 2, from mid-May onwards), conditioned by new stringent rules aimed at minimizing the risk of contagion, certainly improved the framework of business expectations, albeit to a lesser extent than expected. 46% of the companies interviewed, in fact, showed further signs of rundown, while 27% were on average (more or less 10% compared to the same period last year).

On a complimentary basis, only 21.6% of the companies announced to resume business by recovering the work lost during the lockdown partly or entirely. Specifically, 18.9% increased their turnover by 18.9%, while only 2.5% totaled a +50% increase. Moreover, the recent rebound of contagion cases can only negatively affect these projections, worsening an already critical picture.

Graphic 4 – Turnover trend during phase 2 compared to the previous year

Year 2020 (in percentage)

Source: Symbola Foundation survey

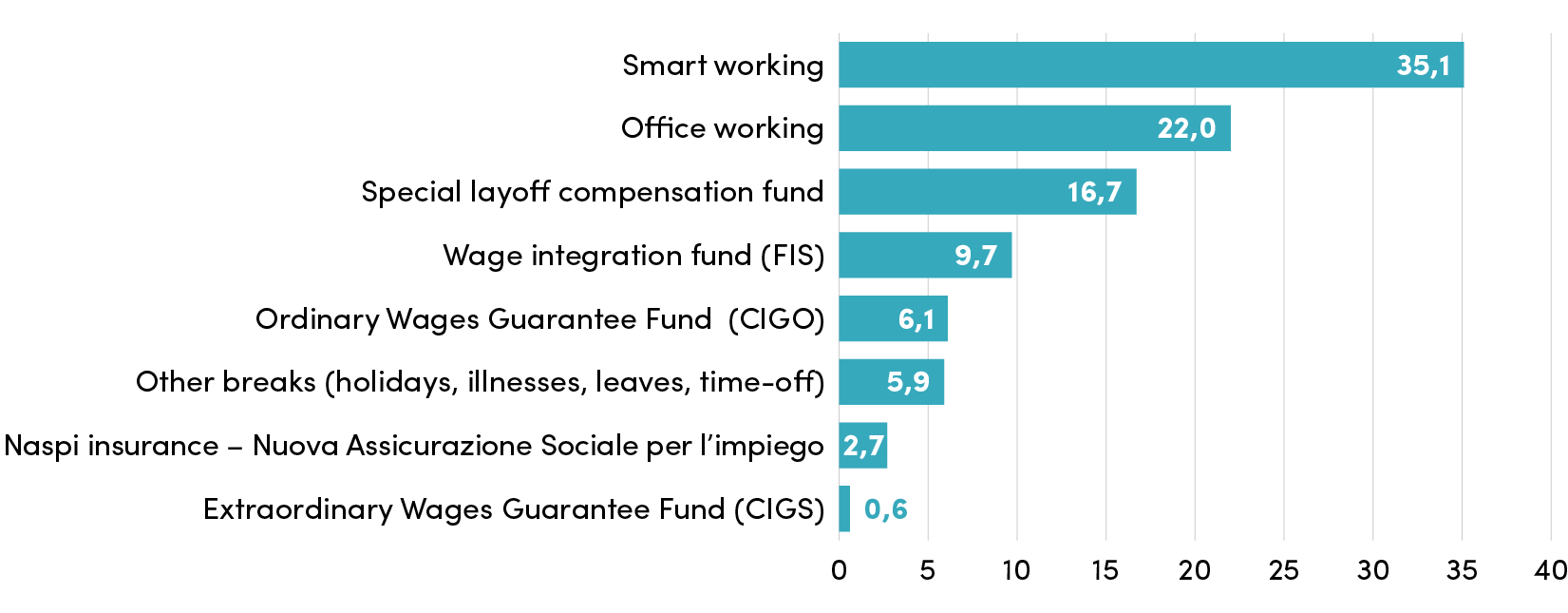

The pandemic and generalized crises have also brought significant organizational innovations that could change the future working models and the world of work. Among these, the intensification of smart working, which allowed most of the tertiary activities to carry on with their activities without affecting the risk of contagion.

Among the employees of audiovisual companies, more than one-third (35.1%) adopted this working method, while 22% continued to work on site. Overall, less than 60% of the workforce was employed during the lockdown thanks to the possibility for companies to resort to various forms of interruption: redundancy funds, wages in derogation (16.7% of the employees of the companies interviewed); wage integration funds (9.7%); ordinary CIG (6.1%); other breaks, such as holidays, illnesses, leaves and time-off (5.9%).

Graphic 5 – Breakdown of audiovisual companies working models in Phase 1

Year 2020 (in percentage)

Source: Symbola Foundation survey

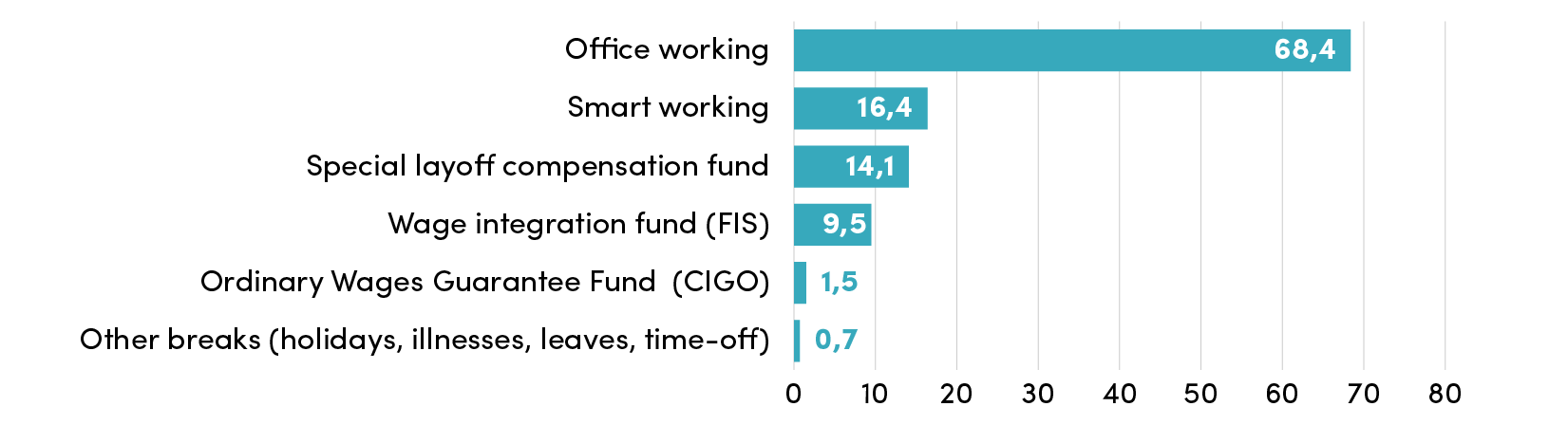

Once the lockdown was over, companies reorganized their businesses by reshaping the working model of their employees. On a total number of employees employed by the companies contacted by telephone, more than two-thirds continued or resumed operating in offices (68.4%), and 16.4% continued smart working. A percentage halved compared to the lockdown period but certainly higher than before the health crisis, suggesting this approach was appreciated.

Graphic 6 – Breakdown of audiovisual companies working models in Phase 2 (May 18-December 31, 2020)

Year 2020 (in percentage)

Source: Symbola Foundation survey

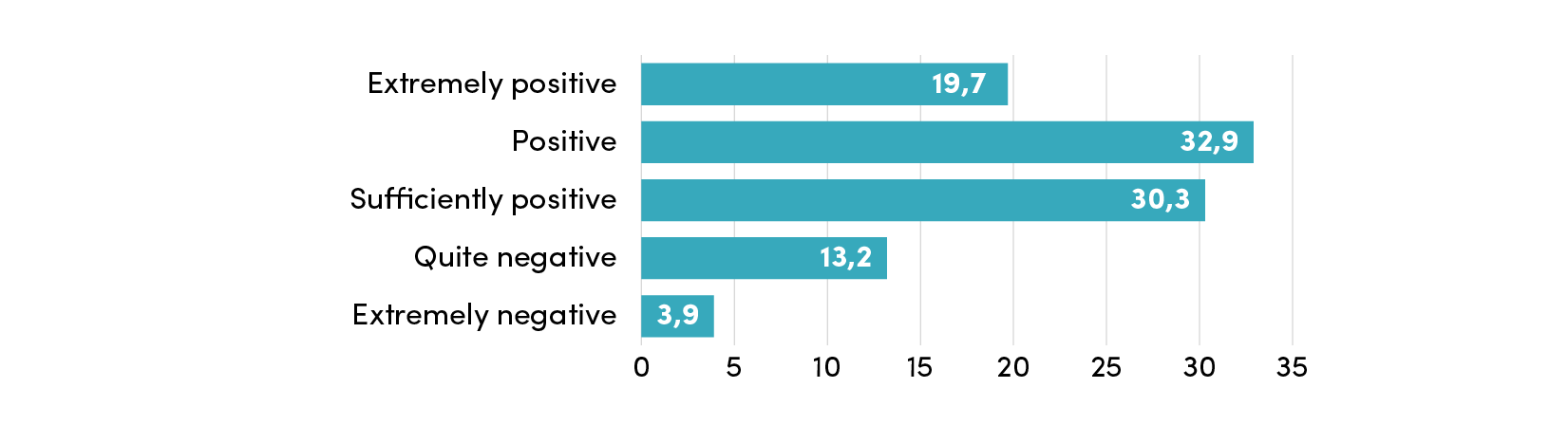

When asked about their smart working experience, more than half of the audiovisual companies indicated a satisfactory level of satisfaction. Specifically, 19.7% of the sample recorded a fairly positive opinion, while the answer given by about one-third of the companies interviewed (32.9%) is “very positive.” Still, 30.3% consider the experience “at a passing grade,” while only a small part seems to have encountered critical issues. 13.2% remarked a “fairly negative” opinion, and the remaining 3.9% “very negative.”

Graphic 7 – Opinion on the smart working experience for the audiovisual companies that adopted it

Year 2020 (in percentage)

Source: Symbola Foundation survey

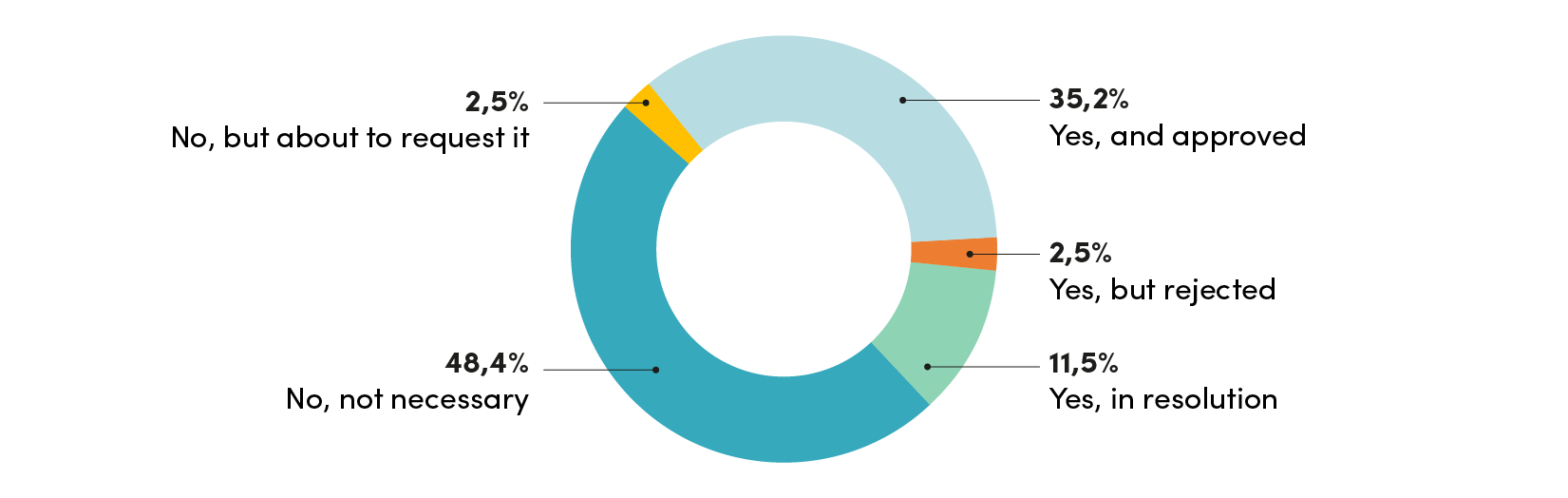

The closure and subsequent resumption of production activities affected the strategies of audiovisual companies, directing them to adopt measures aimed at containing rundown and preventing financial imbalances. Many companies applied to the banking system for new credits, favored by government loan guarantee tools. The liquidity induced in the system, guaranteed by public action, supported relations between banks and businesses, so much so that over half of the companies in the sector decided to apply for new credit lines, often with success.

Graphic 8 – Bank credit line requests to tackle the health crisis

Year 2020 (in percentage)

Source: Symbola Foundation survey

Considering the share of applicants stood at 49.1%, what immediately catches the eye is that the banks refused only 2.5% (or 5% of applicants). For 35.2%, the approval has already taken place, while 11.5% of the companies are waiting for a rapid resolution by the chosen credit institution. Among those that have not yet requested new credit lines, 2.5% plan to do so in the near future, a share that is certainly meant to grow due to the October 2020 restrictions related to the second pandemic wave.

Graphic 9 – Redefinition of payment terms to suppliers and landlords due to the health crisis

Year 2020 (in percentage)

Source: Symbola Foundation survey

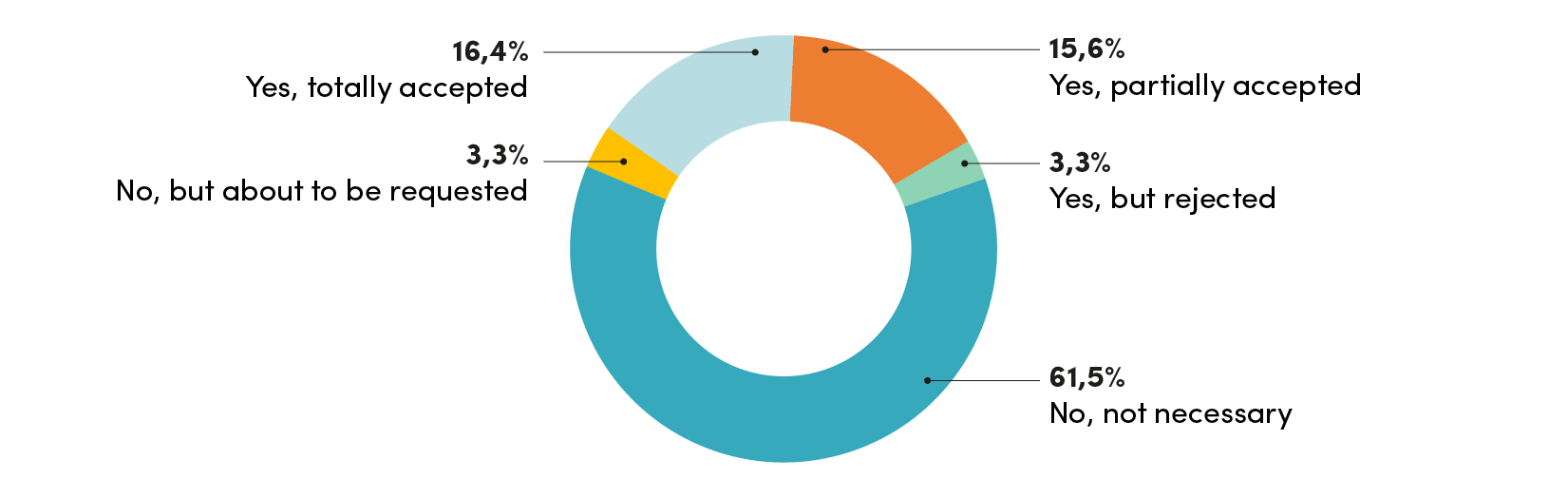

Another road the audiovisual companies elected to limit losses was to re-negotiate their previous conditions with suppliers and landlords. In this case, the percentage of active companies was nearly one-third, 16.4% of which report that their request was fully accepted, while 15.6% show a partial affirmative response. Only 3.3% suffered a total refusal, proof of how in difficult times relationships work in the interest of flexibility.

Graphic 9 – Companies reorganization measures adopted or in the process of being adopted

Year 2020 (in percentage; multiple choice)

Source: Symbola Foundation survey

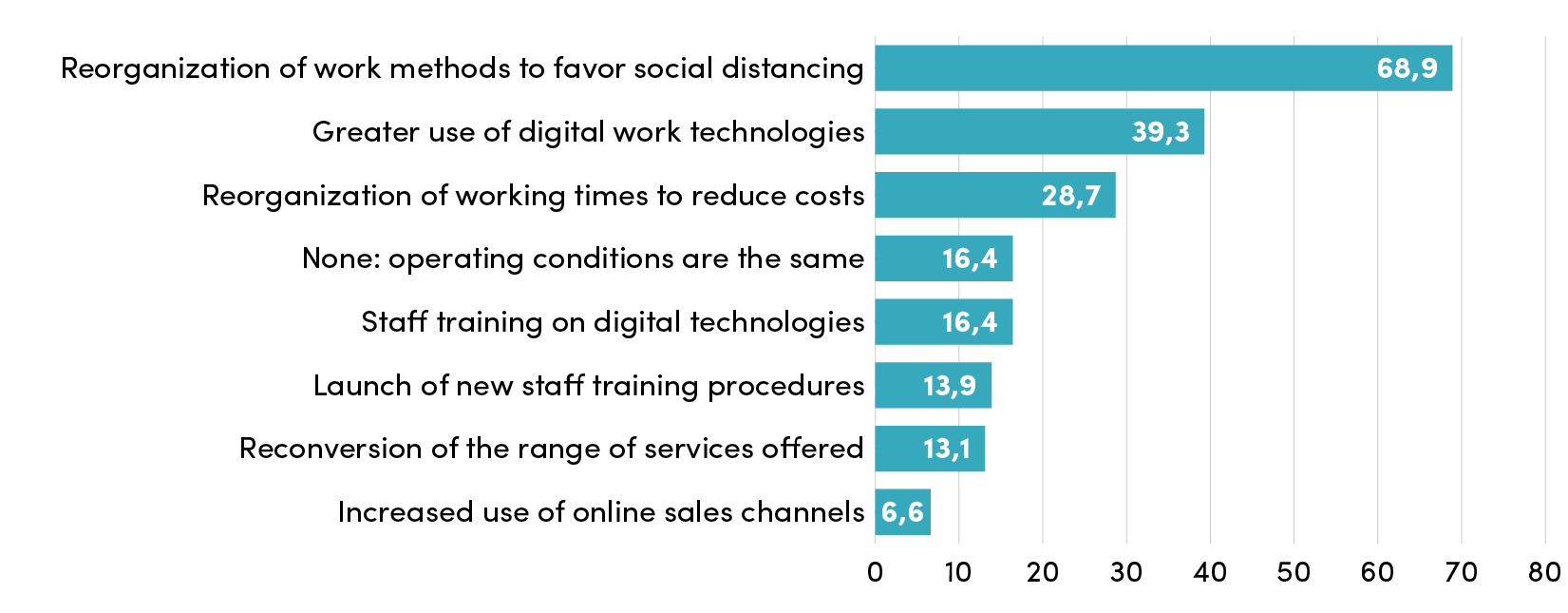

Audiovisual companies eventually showed particular attention to strategies for reorganizing working models aimed at distancing. 68.9% of the companies interviewed took action in this regard. The digitization front was also central, applied to smart working and digital work (39.3%), ICT training (16.4%), or online sales channels (6.6%). On the other hand, few companies thought about reconverting their range of services on the market, underrating the pandemic implications in the medium term (13.1%).

Graphic 10 – Public measures to support companies through the health crisis

Year 2020 (in percentage)

Source: Symbola Foundation survey

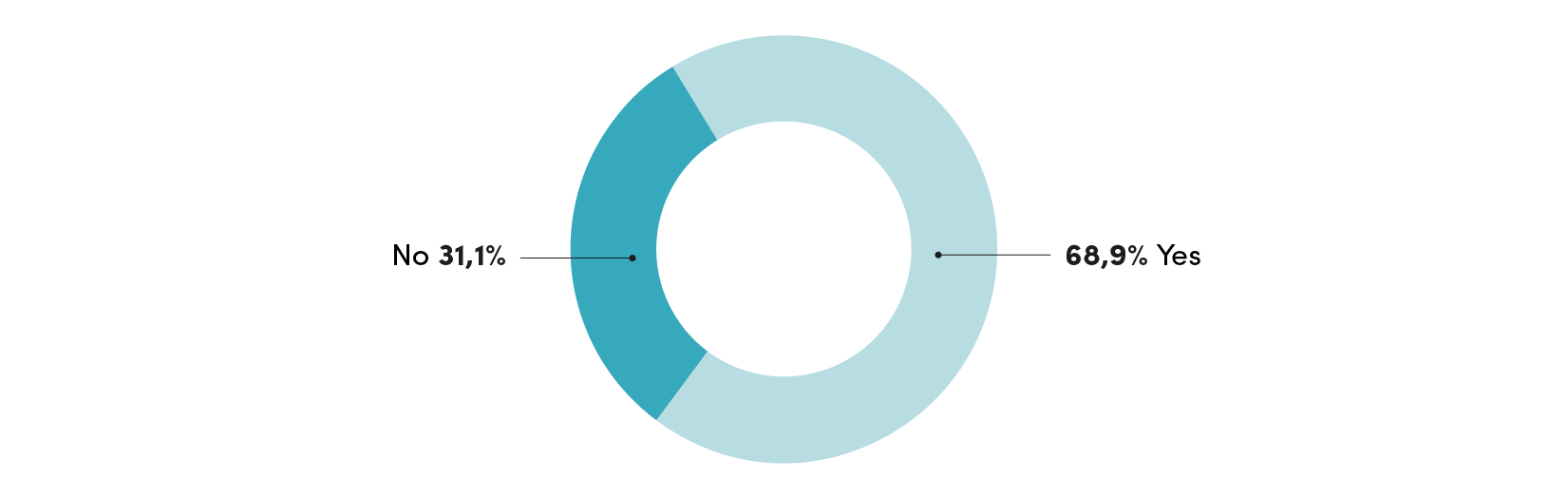

In general, more than two-thirds of businesses benefited from concessions and public support tools promised by the government.

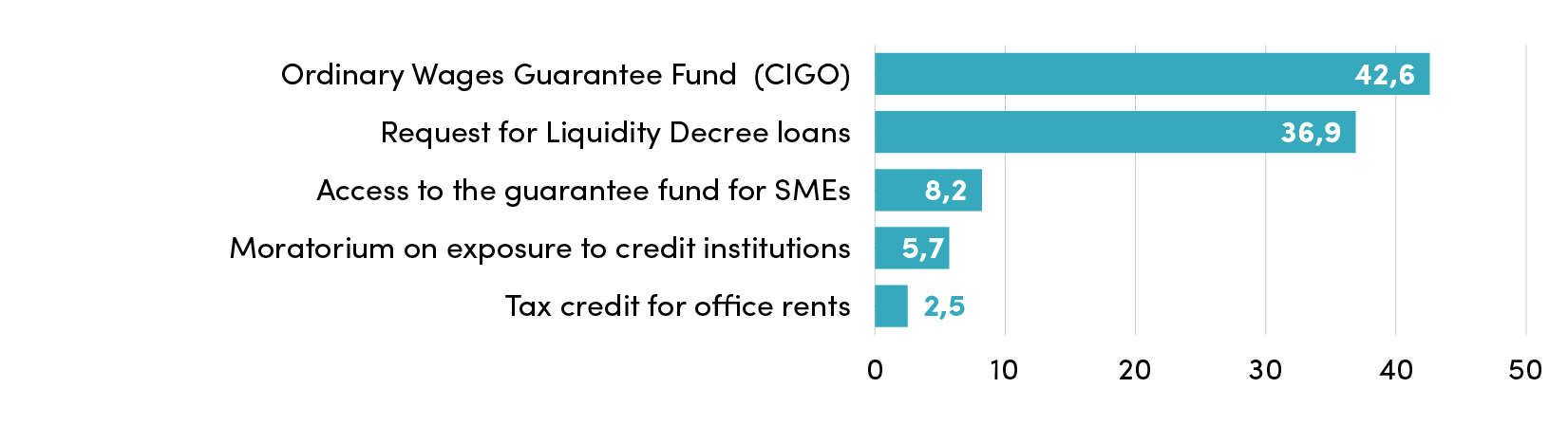

The most popular measures were the Redundancy Fund (Cassa integrazione Guadagni, CIG) or wage subsidies (Fondo di Integrazione Salariale, FIS), followed by tools provided for by the Liquidity Decree (36.9%). Less widespread but nonetheless strategic for the sector’s stability were the measures for accessing the SME Guarantee Fund (8.2%), designed to support bank/business relationships in such a difficult time. Finally, the use of moratoria for bank exposures (5.7%) and tax credits for shop leases (2.5%) were marginal.

Graphic 11 – Breakdown of public measures to support the health crisis by type

Year 2020 (in percentage; multiple choice)

Source: Symbola Foundation survey

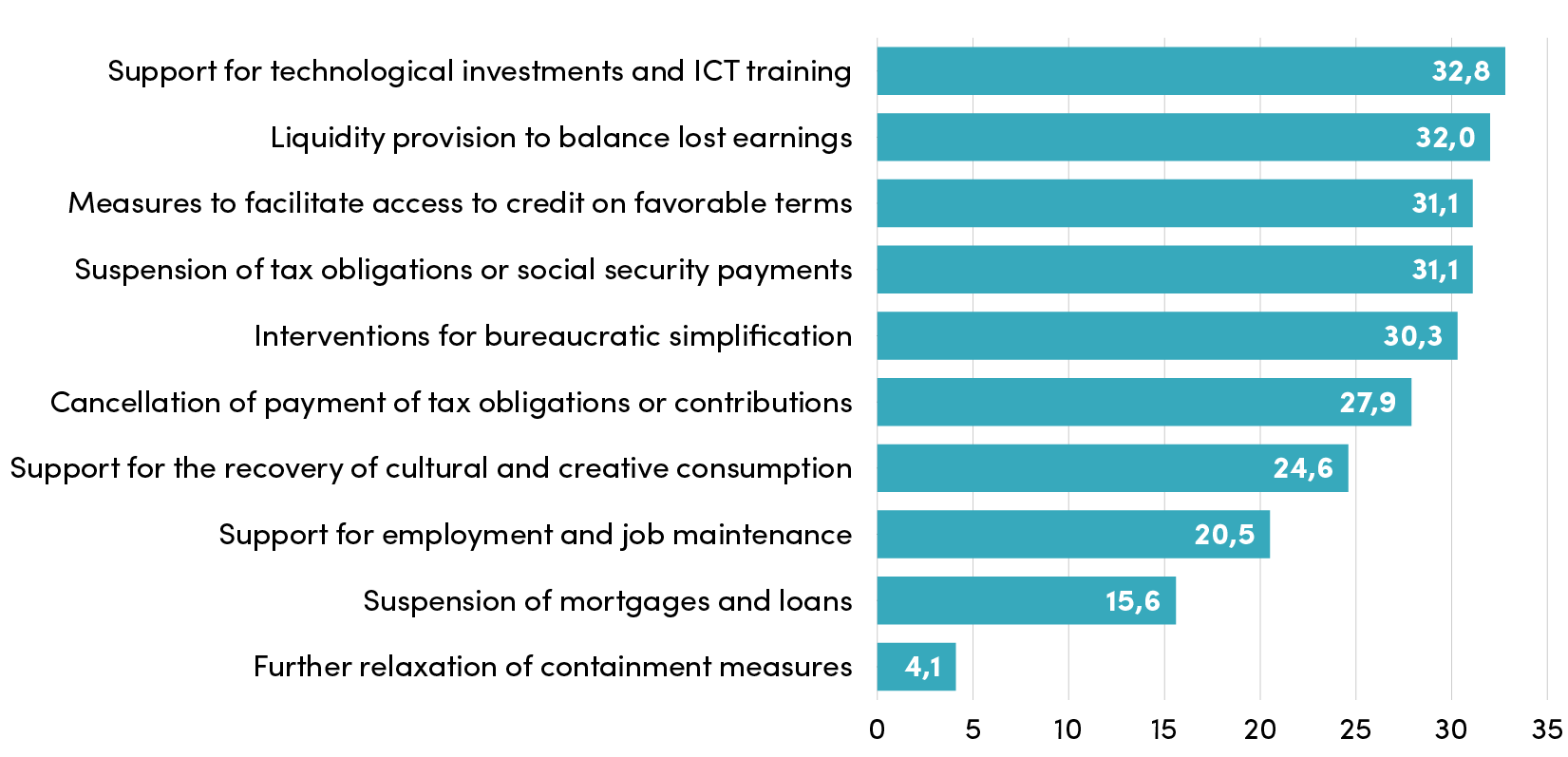

After the first wave of the health crisis and the subsequent measures implemented by the government, it was possible to rate companies’ approval, which happens to be valuable information, especially due to the resumption of infections that should characterize the upcoming months. When interviewed on which measures required larger investments, the audiovisual companies gave varied answers. In particular, five actions seem to prevail for more than 30%: support for technological investments; liquidity provision to balance lost earnings; simpler credit access; suspension of tax obligations; easing on bureaucratic burdens. Overall, a mix of measures to support the drawbacks and tools and set up relaunch strategies to allow the sector to face the future in the crisis aftermath.

Graphic 12 – Public measures to support the health crisis in need of investment

Year 2020 (in percentage; multiple choice)

Source: Symbola Foundation survey