Employment and wealth growth: 2019 and the consequences of the healthcare crisis

The 2019 outcome for the audiovisual sector was substantially flat, as for the Italian economy in general, while the 2020 wave has strongly impacted the industry, with greater effects than what took place in the rest of the domestic economy.

This is evident in the national estimates, carried out in a framework consistent with the official Istat procedures that reveal yearly figures concerning wealth and employment.

Both in terms of wealth and employment, the audiovisual sector has paid heavily for the effects of the 2020 pandemic crisis: the decrease in value added at current prices was -12.1% compared to the total economy figure of -7.2%, while the reduction in employment was -7.9% whereas the overall figure was much more contained, due to the different sectors featuring different trends.

Entering the industrial trends, the unprecedented impact of the pandemic explosion fell mainly on Theatrical activities (Ateco 5914), which recorded a loss of -42.0% in terms of wealth and -31.3% employment. Programming and TV broadcasting activities (Ateco 6020) also experienced a -7.8% loss in gross product which was accompanied by a -6.4% on the employment side.

Production (Ateco 5911) mainly paid in terms of wealth (-10.1%), while employment losses were contained (-3.2%), perhaps thanks to the post-lockdown resumption of activities.

Table 3 – Breakdown of the audiovisual core wealth and employment by Ateco classification

Year 2019 (absolute value and percentage variation)

WEALTH

| Variations % | ||||

| Ateco | Ateco Classification | M-Euros | 2019-’20 | 2011-’20 |

| 5911 | Theatrical, video & TV production activities | 1.268,4 | -10,7 | -18,8 |

| 5912 | Theatrical, video & TV post-production activities | 218,4 | -6,9 | -2,1 |

| 5913 | Theatrical, video & TV distribution activities | 119,2 | -3,0 | 16,5 |

| 5914 | Theatrical activities | 315,7 | -42,0 | -44,8 |

| 6020 | TV programming and broadcasting activities | 2.579,1 | -7,8 | -19,7 |

| TOTAL AUDIOVISUAL CORE | 4.500,8 | -12,1 | -20,6 | |

| TOTAL ECONOMY | 1.490.613,8 | -7,2 | 0,7 | |

EMPLOYMENT

| Variations % | ||||

| Ateco | Ateco Classification | Employee coun | 2019-‘20 | 2011-‘20 |

| 5911 | Theatrical, video & TV production activities | 14.951 | -3,2 | -11,2 |

| 5912 | Theatrical, video & TV post-production activities | 2.251 | -1,4 | 8,2 |

| 5913 | Theatrical, video & TV distribution activities | 1.240 | 0,1 | 25,9 |

| 5914 | Theatrical activities | 3.851 | -31,3 | -4,5 |

| 6020 | TV programming and broadcasting activities | 22.502 | -6,4 | -25,1 |

| TOTAL AUDIOVISUAL CORE | 44.795 | -7,9 | -17,0 | |

| TOTAL ECONOMY | 24.978.300 | -2,1 | 0,5 | |

Source: Symbola Foundation

In descending order, as to the extent of the impact, Post-production (Ateco 5912) reveals a reduced impact, given the possibility of this class to bring on its activity (and due to works carried out in periods prior to lockdown), with a drop in added value of -6.9%, and a reduction in employment of -1.4%.

The sector least affected by the effects of the annus horribilis was Distribution (Ateco 5913), with a wealth loss of -3.2%, even showing a positive sign (albeit only one tenth of a percentage point) in terms of employment.

The results of just one year determined negative effects that can be noticed also in a broader temporal dimension such as the decade 2011-2020. Reading the 2011-2019 results, the overall variation in wealth and employment was computed in a loss of ±10%, values that fly to -20.6% in 2011-2020 for wealth and -17% for employment.

From the point of view of the subsectors that make up the audiovisual core, the 2020 earthquake worsened the conditions of some classes (Production, -18.8%, TV programming and broadcasting, -19.7% as for wealth). In the case of Theatrical, the epidemiological crisis hit the sector strongly, bringing the decade balance to -44.8% in terms of wealth and -4.5% in terms of employment, whereas the results for the 2011-2019 period showed a much less serious -4.8% in the first case (wealth) and even an extremely positive figure in the second (+39.0% employment).

Beyond the 2020 results, the audiovisual core suffers from an evident problem concerning the composition of the forces at stake, since even the most dynamic fail to affect the whole supply chain, at least for now. On the other hand, the cornerstone subsectors continue to suffer, especially Theatrical.

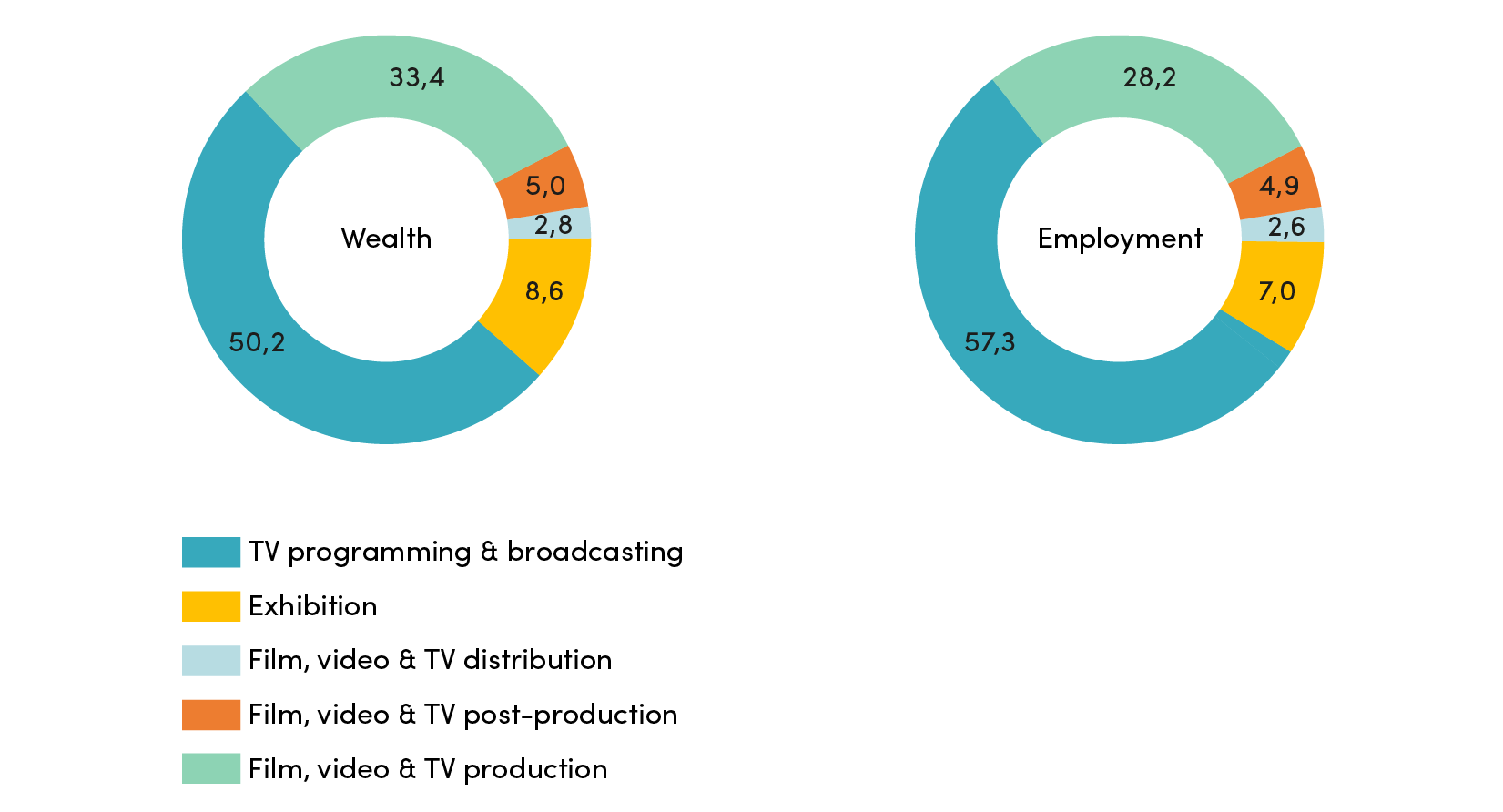

Theatrical distribution contributes to the wealth and employment produced by the supply chain for values below three percent (2.8% and 2.6%, respectively). Post-production (Ateco 5912) has more encouraging dynamics, although it affects the total supply chain by only 5%, both in terms of wealth and employment.

The struggle experienced in recent years by the theatrical sector, combined with the strong impact of the pandemic, has reduced its impact on the supply chain, both in terms of wealth and employment, with percentages dropping to 8.6% and 7.0%, respectively.

Production (Ateco 5911) accounts for a share of 33.4% in terms of gross product and 28.2% of employment, while TV programming and broadcasts (Ateco 6020) account for 50.2% of the total wealth of the core, share which rises to 57.2% for employment.

The summary that comes from the numbers reported above highlights all the frailties and struggle faced by the audiovisual sector in 2020, an industry that shows far worse results than the entire economy.

Presently, (autumn 2021), the picture seems to improve, although a full recovery appears to be strongly conditioned by the evolution of the health emergency and the effectiveness of the vaccine administration campaign. Not surprisingly, culture – and therefore also the audiovisual supply chain – finds plentiful space within the framework of measures proposed by the government in its Piano nazionale di Ripresa e Resilienza (National Recovery and Resilience Plan), which to date seems to be the main source of hope to return to what analysts describe as the “new normal.”

Breakdown of the audiovisual core wealth and employment by productive field

Year 2019 (wealth and employment in percentage)

Source: Symbola Foundation

2019 vs 2020: Self-employed workers/Employed

2019: 119.312 people was engaged in audiovisual activities

| Self-employed workers (Individuals) | 52.546 |

| Employed | 45.461 |

| Managers | 14.491 |

| Former Enpal employees outside the core perimeter | 4.040 |

| Entrepreneurs | 2.774 |

| TOTAL | 119.312 |

2020: 111.287 people was engaged in audiovisual activities

| Self-employed workers (Individuals) | 47.955 |

| Employed | 42.203 |

| Managers | 14.509 |

| Former Enpal employees outside the core perimeter | 3.810 |

| Entrepreneurs | 2.810 |

| TOTAL | 111.287 |

(7) The assessments on wealth and employment (i.e. by workplace), consistent with the most current National Accounting frameworks (national and territorial), are the result of elaborations carried out starting from the ASIA archives of Istat, integrated and updated with data from Infocamere which offers the possibility of building to private employment, integrated with the public component, starting from data based on the Istat census for institutions. The economic parameters are always obtained from the elaboration of Istat data, this time relating to surveys on company accounts.